Tips, Overtime, and a New Senior Deduction: Don’t Wait Until Filing Season to Get Ready

June 29, 2026

We’re now halfway through 2026, which makes this the perfect moment to look at three of the most talked-about deductions from the One, Big, Beautiful Bill Act—the breaks for tips, overtime, and seniors. These provisions are already in effect for 2025 through 2028, but the rules for 2026 come with a twist: how your income gets reported now determines whether you can actually claim the deduction. A little planning today can save you a headache and real money next spring.

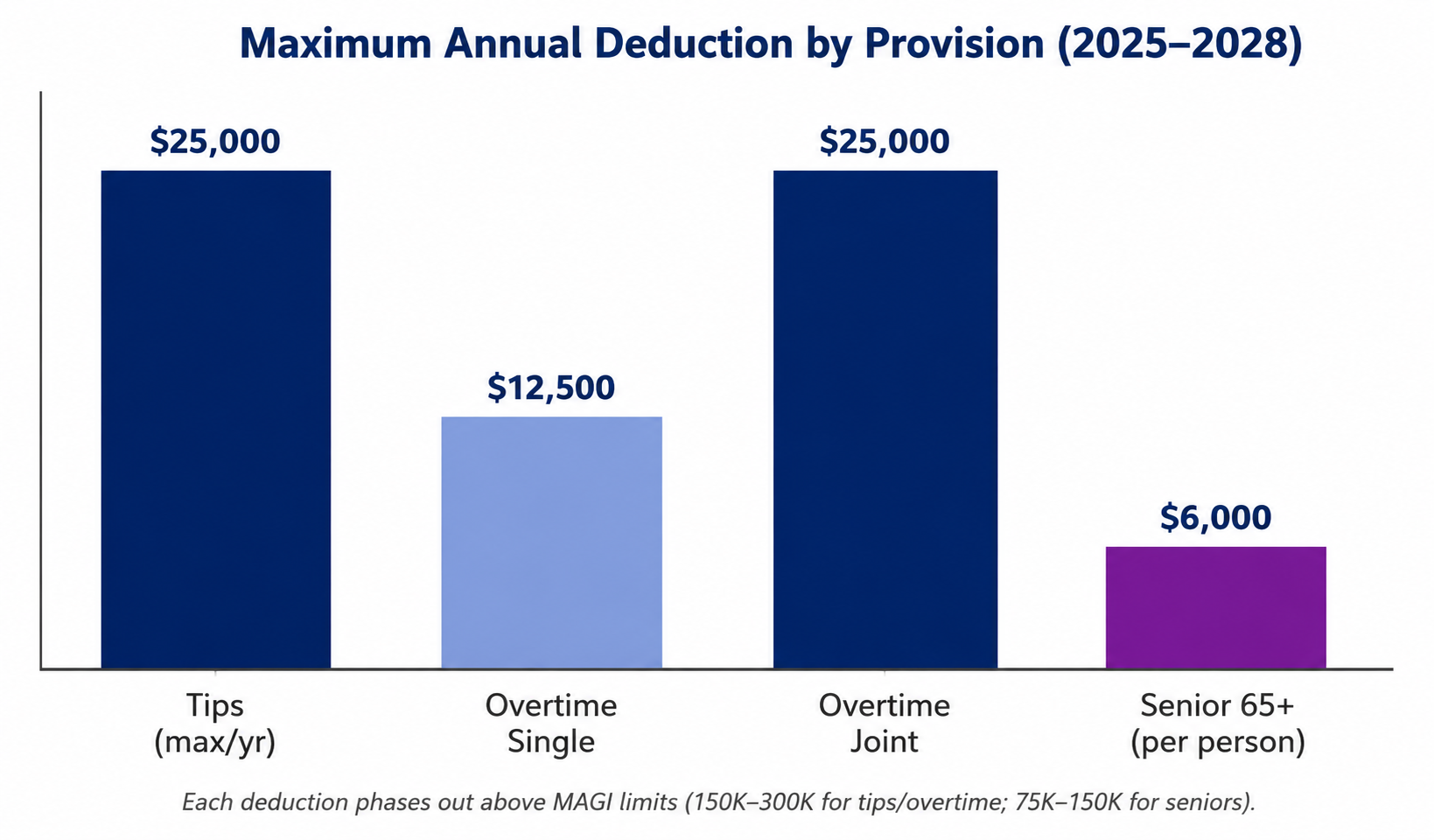

How the three deductions compare. Caps apply per year and phase out above the income limits shown.

The “No Tax on Tips” Deduction

If you or your employees work in a tipped occupation, this one is worth understanding well. For 2025 through 2028, eligible workers can deduct qualified tips received in occupations that the IRS lists as customarily and regularly tipped. The deduction is capped at $25,000 per year. For self-employed individuals, it can’t exceed the net income from the business in which the tips were earned.

There’s an income limit to keep in mind. The deduction begins to phase out once modified adjusted gross income, or MAGI, tops $150,000 for single filers or $300,000 for joint filers. Above those levels, the benefit shrinks and eventually disappears.

The key takeaway for both workers and the businesses that employ them: tips need to be tracked and reported accurately. A deduction is only as good as the records behind it.

The Overtime Deduction—and Why 2026 Is Different

The overtime break works a little differently from how many people first assume. You don’t get to deduct all of your overtime pay—only the premium portion. That’s the extra “half” in time-and-a-half. So if your regular rate is $20 an hour and overtime pays $30, the deductible amount is the $10 difference, not the full $30.

The annual cap is $12,500 for single filers and $25,000 for joint filers, and it phases out at the same MAGI thresholds as the tip deduction—$150,000 single, $300,000 joint.

Here’s the part that matters most right now. Beginning with the 2026 tax year, Forms W-2, 1099-NEC, 1099-MISC, and 1099-K are being updated to report qualified overtime compensation separately. Only overtime that’s separately reported on these forms will be deductible for 2026. In plain terms: if the premium portion of overtime isn’t broken out on the form, the deduction may be off the table.

For small business owners, this is a payroll and bookkeeping issue you’ll want to address before year-end—not in January. Make sure your payroll system or provider is set up to track and separately report qualified overtime for 2026. For employees, it’s worth confirming with your employer that overtime is being captured correctly so your W-2 reflects it next year.

For businesses and individuals who want help reviewing their setup before filing season, SAPIR EA provides tax services designed to help identify planning opportunities before they become last-minute problems.

A Bonus Deduction for Taxpayers 65 and Older

The third provision is refreshingly simple. For 2025 through 2028, individuals age 65 and older can claim an additional $6,000 deduction. It’s per eligible person, so a married couple where both spouses qualify can deduct up to $12,000.

This one phases out at lower income levels than the others—MAGI above $75,000 for single filers and $150,000 for joint filers—so it’s aimed squarely at middle-income retirees and older workers. Importantly, you can claim it whether you itemize or take the standard deduction, which makes it accessible to a broad group of older taxpayers.

New This Summer: “Trump Accounts” for Kids

The same law created an entirely new savings vehicle for children, informally known as a Trump Account, and it’s especially relevant right now: contributions can’t be made until July 4, 2026. If you’re a parent—or a business owner thinking about employee benefits—this is worth a close look.

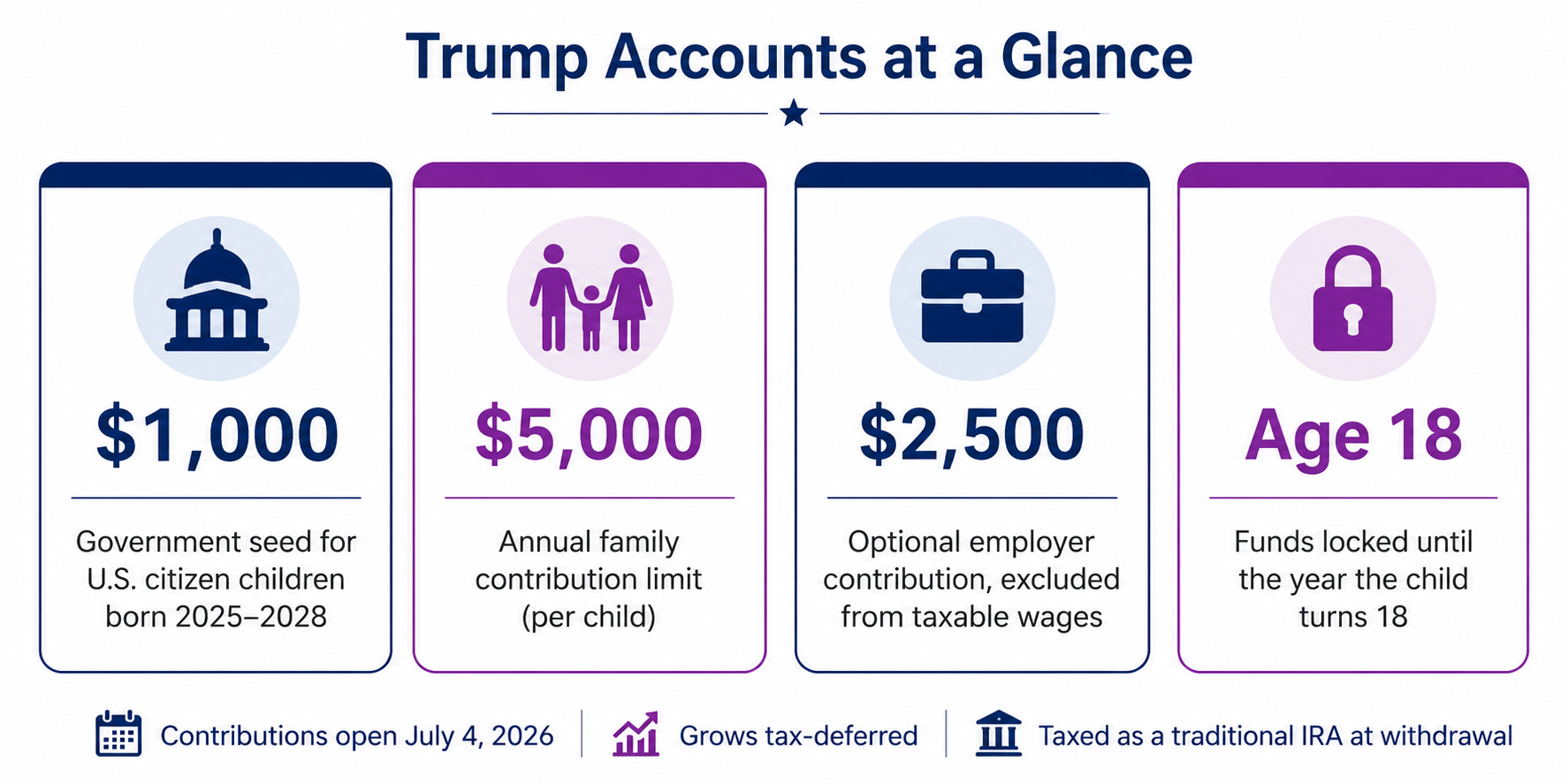

Trump Accounts at a glance: seed contribution, limits, and key rules.

A Trump Account is a tax-deferred account that functions much like a traditional IRA, opened in a child’s name. As part of a pilot program, the federal government will deposit a $1,000 seed contribution for eligible U.S.-citizen children born between January 1, 2025 and December 31, 2028 who have a valid Social Security number. That seed doesn’t count against the annual contribution limit.

Beyond the seed, family and friends can contribute up to $5,000 per year per child, a figure that will be indexed for inflation. These contributions aren’t tax-deductible, but the money grows tax-deferred. There’s also an employer angle worth noting: employers may contribute up to $2,500 per year toward an employee’s child’s account, and that amount is excluded from the employee’s taxable wages. The $2,500 counts within the $5,000 annual cap.

Funds generally stay locked until January 1 of the year the child turns 18. After that, the account is treated like a traditional IRA—withdrawals of pre-tax amounts and earnings are subject to ordinary income tax, and the usual IRA rules apply. In short, it’s a long-term, tax-advantaged head start rather than a flexible savings account.

Two practical notes. First, you don’t need to rush on July 4—the $1,000 seed is tied to the child’s eligibility, not a first-come deadline, so there’s time to choose the right provider. Second, business owners should weigh whether offering the $2,500 contribution makes sense as a recruiting and retention perk, since it’s a tax-efficient benefit for employees with young children.

Practical Steps to Take This Summer

A few things you can do now, while there’s still plenty of runway in 2026:

- Check your recordkeeping. Tips and overtime both depend on clean, accurate records. If you’re self-employed and earning tips, keep a contemporaneous log rather than reconstructing numbers later.

- Talk to your payroll provider. Business owners should confirm their systems will separately report qualified overtime on 2026 W-2s and 1099s. This is the single most common place the overtime deduction will be lost.

- Run a mid-year income estimate. Because all three deductions phase out based on MAGI, knowing roughly where your income will land helps you plan—and may open the door to moves like retirement contributions that lower MAGI.

- Coordinate with estimated payments. If these deductions meaningfully change your expected tax, you may be able to adjust your remaining quarterly estimated payments rather than overpaying all year.

These steps are part of proactive tax planning and preparation, especially for business owners, self-employed workers, retirees, and households near the income phaseout limits.

The Bottom Line

The tip, overtime, and senior deductions can deliver real savings—but the 2026 reporting requirements mean the work happens before you file, not after. The middle of the year is the ideal time to make sure your records and payroll setup are ready, and to confirm you fall within the income limits.

If you’d like help figuring out how these provisions apply to your specific situation—whether you’re a business owner setting up payroll reporting or an individual wondering if you qualify—the team at SAPIR EA is here to help. Reach out and we’ll walk through it together.

Need Help Understanding How These Deductions Apply to You?

Whether you are a business owner, employee, retiree, or self-employed taxpayer, SAPIR EA can help you review your situation and prepare before filing season arrives.

Contact UsThis article is provided for general informational and educational purposes only and does not constitute individualized tax, legal, or financial advice. Tax rules are complex and depend on your specific circumstances. Please consult a qualified tax professional before making decisions based on this information.