2026 Tax Changes You Can't Ignore: How OBBBA Impacts S-Corp Owners, Side Hustlers, and High-Earners

June 24, 2026

If you own a business, run a side hustle, or earn a high income, the 2026 tax changes flowing from the One Big Beautiful Bill Act (OBBBA) deserve a spot at the top of your to-do list. Signed into law on July 4, 2025, OBBBA represents the most significant set of tax law changes in years — and unlike the temporary cuts that were scheduled to expire, many of these provisions are now permanent. That permanence is exactly why smart tax planning starting now can pay off for years to come.

Below is a plain-English walkthrough of what changed, who it affects most, and the tax-saving strategies worth discussing with your tax professional before year-end.

A Quick Overview of OBBBA

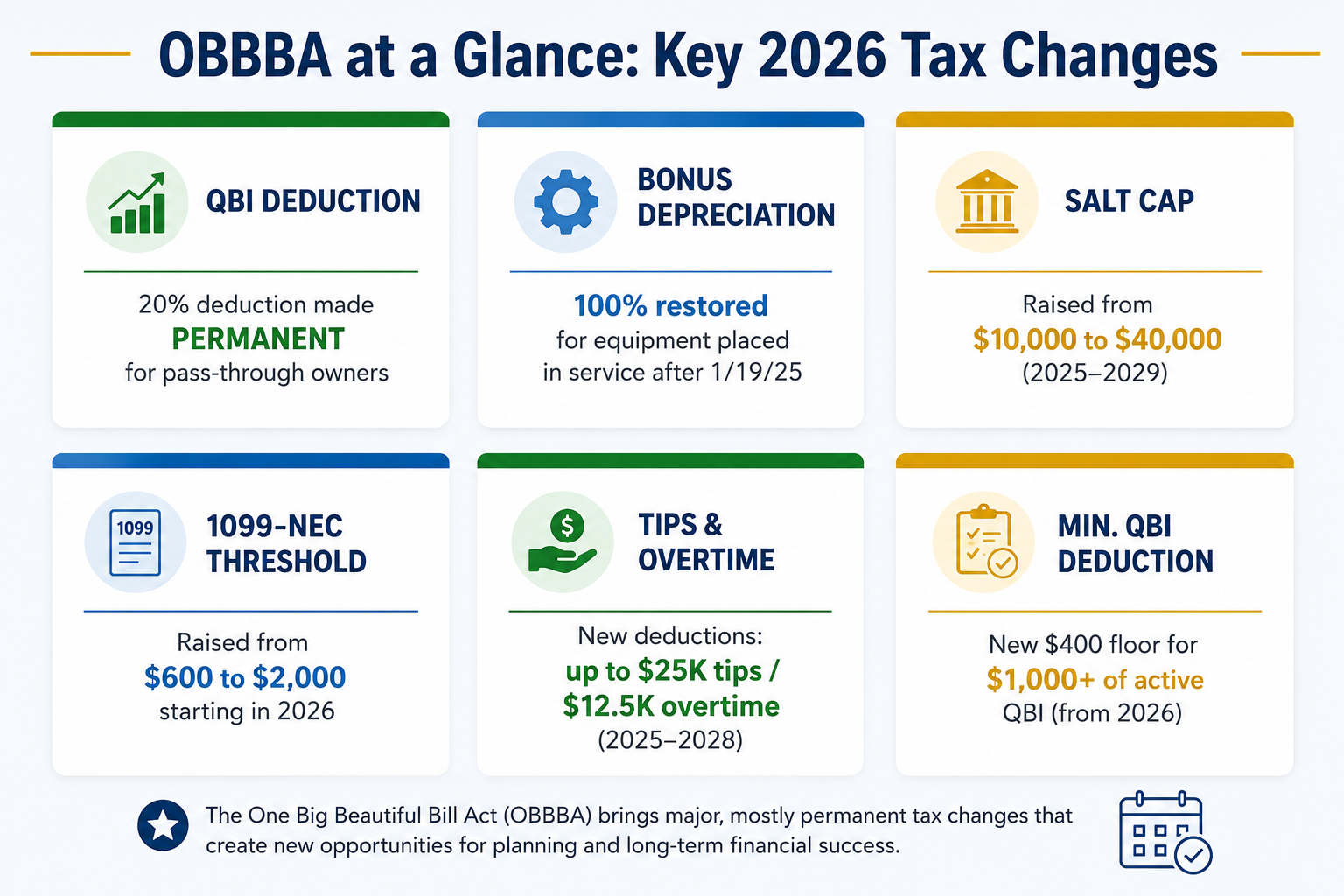

The One Big Beautiful Bill Act did three big things at once: it locked in the lower individual rates that were set to sunset, it sweetened several deductions for business owners, and it adjusted reporting rules that touch nearly everyone with self-employment income. For pass-through businesses, the headline is that the qualified business income deduction is now permanent. For individuals, new deductions for tips and overtime, a much larger state-and-local-tax cap, and restored 100% bonus depreciation all reshape the planning landscape.

Because these 2026 tax changes interact with each other, the people who benefit most are the ones who plan ahead rather than react in April. Let's break it down by who you are.

S-Corp Owners: Permanence Creates Planning Opportunity

For S-Corp owners, the most important piece of OBBBA is the permanent extension of the qualified business income deduction under Section 199A. Previously scheduled to expire after 2025, the 20% deduction is now a permanent fixture of the tax code. That single change removes a cloud of uncertainty that has hovered over small business taxes for years and makes long-term S-Corp tax planning far more reliable.

OBBBA also widened the income range over which the deduction phases in. Beginning with the 2026 tax changes, the phase-in range expands from $100,000 to $150,000 for joint filers and from $50,000 to $75,000 for everyone else. In practice, that means more S-Corp owners — especially those in specified service businesses like consulting, law, and accounting — keep more of their deduction across a wider band of income.

The second gift for business owners is the permanent return of 100% bonus depreciation for qualifying equipment placed in service after January 19, 2025. Instead of watching that benefit phase down to 20% in 2026 as previously planned, you can once again deduct the full cost of machinery, vehicles, and equipment in the year you put them to work. For a growing S-Corp, that's a powerful lever — but only if purchases are timed thoughtfully as part of your tax planning, not rushed for the sake of a deduction.

A reminder that has not changed: S-Corp owners still must pay themselves “reasonable compensation” through payroll. The larger QBI deduction makes the wages-versus-distributions balance even more worth modeling, because your salary level directly affects the size of your deduction. This is precisely the kind of calculation where a tax professional and clean bookkeeping earn their keep. Solid books throughout the year — not a shoebox of receipts in March — are what make these tax-saving strategies actionable.

Side Hustlers: New Reporting Rules and a Minimum Deduction

If your income comes from freelancing, gig work, or a weekend business, two OBBBA provisions directly affect your side hustle taxes.

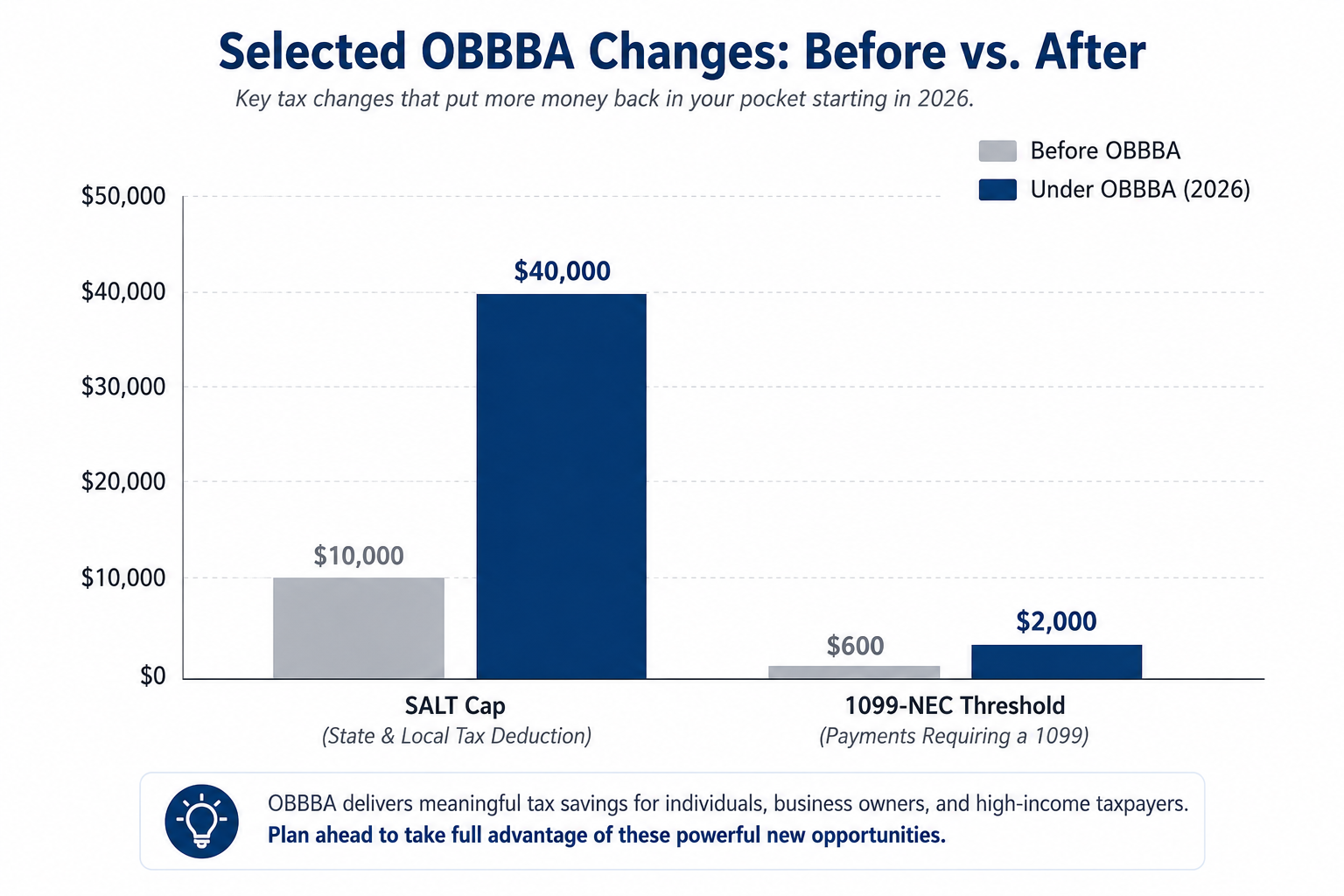

First, the reporting thresholds changed. The Form 1099-NEC and 1099-MISC threshold rose from $600 to $2,000 for payments made in 2026, and it will adjust for inflation going forward. Separately, the Form 1099-K threshold reverted to its older, higher level of more than $20,000 and 200 transactions, replacing the much lower thresholds that had been planned.

Here's the catch that trips people up every year: these are only the levels at which someone must send you a form. They have nothing to do with whether your income is taxable. All of your earnings are still reportable, even the $1,500 client who never issues a 1099 and the $300 you collected through a payment app. If your net self-employment earnings hit $400 or more, you owe self-employment tax and must file. Good bookkeeping is your friend here — track every dollar regardless of what forms arrive, because the IRS expects you to.

Second, the One Big Beautiful Bill Act added a new minimum qualified business income deduction. Starting in 2026, a taxpayer with at least $1,000 of QBI from an active trade or business can claim a minimum deduction of $400, even if the usual calculation would produce less. For smaller side hustles, that's a modest but welcome floor — and a reason to make sure your activity is structured and documented as an active business.

Side hustlers are also the group most likely to get blindsided by estimated taxes. With no employer withholding, you're responsible for paying the IRS throughout the year. Underpaying triggers penalties, so building estimated taxes into your quarterly routine is one of the simplest tax-saving strategies available to anyone with self-employment income.

High-Income Taxpayers: The SALT Cap Changes Everything

For high-income taxpayers, the most consequential of the 2026 tax changes is the expanded cap on state and local tax deductions. OBBBA raised the SALT cap from $10,000 to $40,000 for 2025 through 2029, with a small annual inflation adjustment. For residents of high-tax states, that's a meaningful increase in itemized tax deductions.

There's a phaseout to watch: the higher cap begins to shrink for households with income above $500,000, though it never drops below the original $10,000 floor. That phaseout creates a real planning band where managing your income — through retirement contributions, charitable timing, or deferral strategies — can preserve more of the deduction. This is fertile ground for tax planning, and exactly where high earners should be running projections rather than guessing.

Two more OBBBA features matter for the broader workforce, though they fade out at higher incomes. The new deductions for tips, up to $25,000, and overtime, up to $12,500 or $25,000 for joint filers, are available from 2025 through 2028 — but only for taxpayers under $150,000 of income, or $300,000 for joint filers. High earners generally won't qualify, which makes income-level awareness part of the planning conversation for households near those thresholds.

Finally, high-income business owners should revisit the QBI phaseout ranges, which OBBBA widened for 2026. The expanded ranges mean some owners who lost the deduction entirely under the old rules may now recover part of it — another reason to re-run the numbers under the new tax law changes rather than assuming last year's outcome still applies.

Turning the 2026 Tax Changes Into a Plan

The common thread across all three groups is that OBBBA rewards preparation. These tax law changes are largely permanent, which means the planning you do now compounds over time instead of resetting each year. A few moves worth putting on your calendar:

- Model your S-Corp salary and distributions against the permanent QBI deduction before setting compensation for the year.

- Time major equipment purchases to make the most of 100% bonus depreciation, while keeping the decision driven by business need.

- Tighten your bookkeeping so every dollar of side hustle income is captured and every deductible expense is documented.

- Set up estimated taxes on a quarterly schedule if you have self-employment income, to avoid penalties.

- Run an income projection if you're near the SALT phaseout or the tips/overtime thresholds, where small shifts change your outcome.

Because everyone's situation is different, this article is general information, not personalized advice. The real value of OBBBA shows up when these provisions are applied to your specific numbers. Working with a qualified tax professional — ideally one who knows your business and keeps an eye on your bookkeeping throughout the year — is the surest way to turn the 2026 tax changes into genuine tax savings rather than a missed opportunity.

The One Big Beautiful Bill Act has reshaped the rules for S-Corp owners, side hustlers, and high earners alike. The sooner you fold these changes into your tax planning, the better positioned you'll be when filing season arrives.

Frequently Asked Questions About the 2026 Tax Changes

When did OBBBA take effect?

The One Big Beautiful Bill Act was signed into law on July 4, 2025. Some provisions applied right away in 2025, while several of the most important 2026 tax changes — such as the expanded QBI phase-in ranges and the new minimum deduction — take effect for the 2026 tax year.

Is the qualified business income deduction really permanent now?

Yes. One of the biggest tax law changes in OBBBA is that the 20% qualified business income deduction under Section 199A is now permanent for pass-through entities, including S-Corp owners, partnerships, and sole proprietors. It is no longer scheduled to expire, which makes long-term S-Corp tax planning far more predictable.

Do I still have to report side hustle income if I don't receive a 1099?

Absolutely. The 1099-NEC threshold rising from $600 to $2,000 and the 1099-K threshold returning to $20,000 and 200 transactions only change when a payer must send you a form. All income remains taxable. If your net self-employment earnings are $400 or more, you must file and pay self-employment tax — which is why good bookkeeping matters for side hustle taxes.

What is the new SALT cap under OBBBA?

The state and local tax deduction cap increased from $10,000 to $40,000 for 2025 through 2029, with a small annual inflation adjustment. For high-income taxpayers above $500,000, the cap phases down but never falls below $10,000. This is one of the most valuable tax deductions to plan around.

Are tips and overtime now tax-free?

Not entirely. OBBBA created deductions of up to $25,000 for tips and up to $12,500 for overtime, or $25,000 for joint filers, available from 2025 through 2028. They phase out for income above $150,000, or $300,000 for joint filers, so many high-income taxpayers won't qualify.

What should S-Corp owners do first?

Start with two tax-saving strategies: model your reasonable compensation against the now-permanent QBI deduction, and time any major equipment purchases to use 100% bonus depreciation. A tax professional who understands your books can run these numbers and turn the 2026 tax changes into real savings.

This post is for educational purposes only and does not constitute tax advice. Consult a licensed tax professional about your specific circumstances.